What the Merger Signals for Permian Produced Water Management

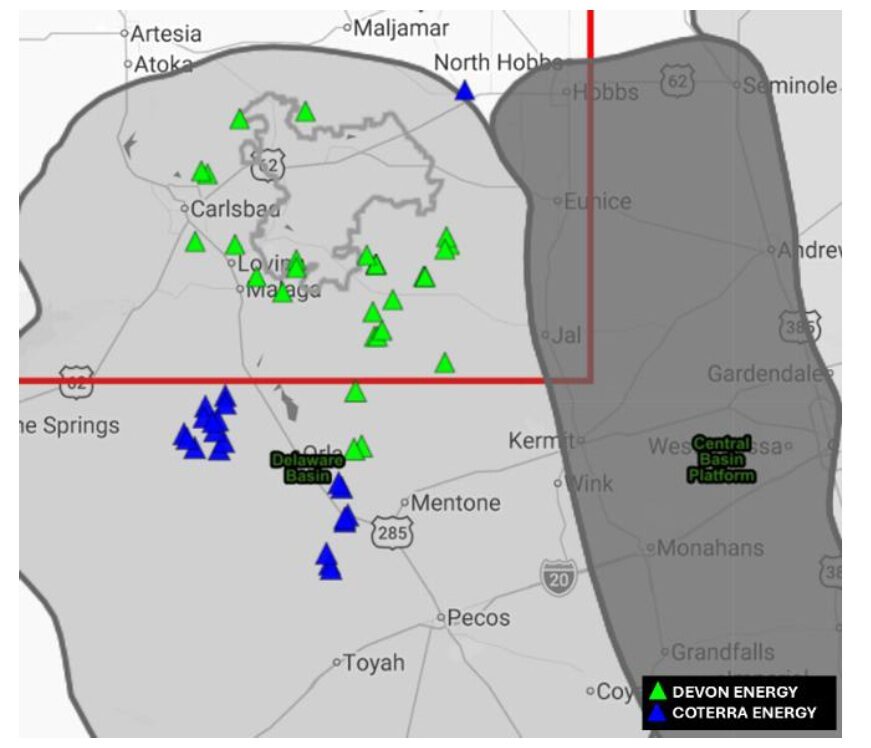

The proposed merger between Devon Energy and Coterra Energy does more than combine acreage and inventory in the northern Delaware Basin. It brings together two distinct produced water systems inside one of the most pressure-sensitive and regulatorily scrutinized regions of the Permian.

In New Mexico’s portion of the Delaware Basin, development strategy is inseparable from water strategy. Disposal capacity, seismic oversight, recycling logistics, and cross-border infrastructure planning are now embedded constraints. As scale increases, so does the complexity of managing those constraints.

Following the transaction, the combined company materially expands its operated footprint across the northern Delaware. Public injection data shows diverging recent trajectories: Devon’s disposal volumes have increased since 2023, while Coterra’s operated injection volumes have remained comparatively stable. Aligning these water profiles will require coordination across development pacing, recycling optimization, third-party disposal access, and pressure-aware planning—particularly in areas where disposal headroom is already tightening.

Recycling as Structural Strategy

Since 2022, recycled produced water has supplied the majority of completion demand for both operators in New Mexico. Devon has notably achieved high recycle utilization, reducing freshwater dependency and buffering against disposal volatility.

The combined footprint presents opportunities to:

- Align recycling specifications and treatment standards

- Optimize facility utilization across contiguous acreage

- Expand recycling capacity where volumes and timing are complementary

But recycling is only part of the equation. Even at elevated recycle rates, significant injection volumes remain. Disposal infrastructure, reservoir pressure conditions, and regulatory thresholds continue to define system capacity. High recycling does not eliminate disposal risk.

Third-Party Infrastructure and Contract Structure Matter More at Scale

Both Devon and Coterra rely meaningfully on third-party water midstream systems. Devon’s long-term infrastructure relationships are well established. Coterra’s third-party footprint is less detailed in public disclosures but consistent with regional market structure.

As these portfolios are integrated, several factors become central:

- Minimum volume commitments (MVCs)

- Cross-border water movement between New Mexico and Texas

- Disposal capacity access versus permitted capacity

- Contract flexibility relative to development cadence

At larger scale, contract structure can either enhance optionality or constrain it. Water midstream alignment will influence capital efficiency, timing, and long-term execution.

The Bigger Signal: Water Is the Operating Constraint

The Devon–Coterra transaction reflects a broader structural shift across the Permian. As upstream consolidation increases acreage scale, water management becomes more central to operational execution and asset valuation.

In the northern Delaware Basin, disposal capacity, pressure management, and recycling reliability increasingly shape:

- Development pacing

- Capital deployment

- Seismic exposure risk

- Long-term inventory economics

For operators, midstream providers, and investors, this merger reinforces reality scale amplifies water complexity. Integration success will depend as much on infrastructure alignment and subsurface pressure awareness as on drilling inventory depth.

B3 Insight’s 2H 2025 Permian Water Market Trends & Forecast includes a detailed M&A feature on the Devon–Coterra transaction, with operator-level water metrics and basin-wide analysis of recycling, disposal capacity, and water strategy implications.