By Patrick Patton, VP of Products, B3 Insight

The Delaware Basin is no longer operating as a closed-loop produced water disposal system. It is becoming the source node in a much larger, basin-scale water network — and the center of gravity is shifting east.

At the 36th Annual Produced Water Society Conference, B3 Insight presented new data outlining the next phase of produced water management in the Permian Basin. The Delaware Basin has crossed a structural threshold, and traditional in-basin disposal strategies are no longer sufficient to accommodate long-term water growth.

The Scale of the Challenge

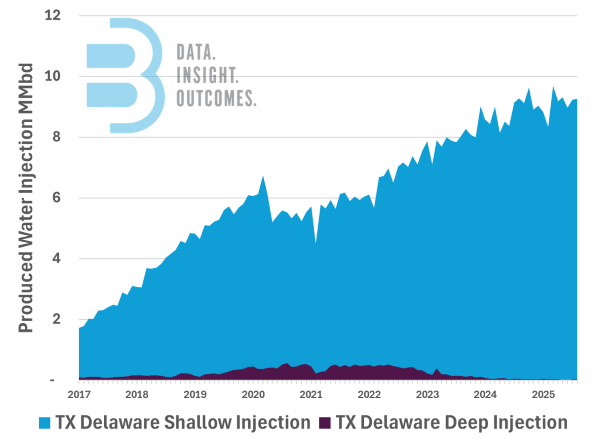

In 2025, the Delaware Basin injected approximately 10.9 million barrels per day of produced water. Since 2017, more than 17 billion barrels have been injected into shallow Delaware intervals in Texas alone — enough water to fill Lake Travis twice. And volumes continue to grow.

B3 Insight forecasts indicate that Delaware Basin disposal demand will increase by approximately 4.8 million barrels per day through 2035, pushing total produced water volumes toward 19 million barrels per day.

This structural growth is driven by sustained oil production and increasing water-oil ratios. Historically, additional disposal demand was met by drilling more saltwater disposal wells. That model is reaching diminishing returns.

Pressure, Not Well Count, Is the Binding Constraint

Injection capacity is governed by two limits: formation pressure and Maximum Surface Injection Pressure (MSIP). As shallow formation pressures increase, available working pressure declines. When formation pressure approaches MSIP, injection rates must be curtailed — regardless of well count. In other words, capacity erodes from within.

Shallow Delaware intervals, particularly the Delaware Mountain Group (DMG), are experiencing measurable pressure increases. As working pressure shrinks, effective disposal capacity declines, even as permitted well counts rise.

At the same time, regulatory policy shapes the rate at which pressure “fill-up” occurs. Reduced MSIP limits can create regulatory capacity constraints before physical limits are reached. Diverging regulatory frameworks between Texas and New Mexico have already reshaped disposal patterns, accelerating cross-border flows.

In 2025, approximately 3.0 million barrels per day of New Mexico-produced water was injected into Texas — a cross-border dynamic that reflects pressure and regulatory asymmetries rather than long-term basin balance.

This cross-border injection functions as a temporary release valve. It does not resolve the structural issue.

The Central Basin Platform Emerges

The Central Basin Platform (CBP) is increasingly positioned as the next frontier for Permian water management.

B3 Insight estimates that more than 2.5 million barrels per day of Delaware-produced water will be injected into the CBP over the next five years. Permit activity in counties such as Andrews and Gaines reflects this directional shift.

This transition is driven by permit behavior, project announcements and economics.

Today, local Delaware saltwater disposal wells in high-pressure corridors can compete with distant disposal projects. However, as shallow formation pressures rise, the economics begin to invert. By 2030, high-pressure Delaware disposal is projected to approach, and exceed in many places, ~$1.20 per barrel all-in, while long-haul distant disposal infrastructure remains near ~$1.12 per barrel of water transported and disposed.

When local disposal becomes more expensive and less reliable, transport becomes critical. Distant disposal is becoming a core design feature of basin-scale water architecture.

A Basin-Scale Management Problem

The industry’s core disposal question is shifting.

It is no longer: Where can the next disposal well be permitted?

It is now: How should pressure be redistributed across the basin?

Distant disposal extends the life of existing Delaware infrastructure by reducing localized pressure accumulation. It rebalances working pressure, slows effective capacity decline, and alters competitive positioning across operators and midstream water companies.

At the same time, new questions emerge:

- Will pressure challenges propagate to the CBP as injection ramps up?

- How will regulatory policy evolve as injection shifts east?

- What mineral and property-right implications accompany expanded CBP disposal?

- How will recycling, discharge, and alternative strategies integrate into a diversified solution set?

Disposal will remain the cornerstone of Permian water management. However, it will not remain geographically concentrated.

Early Innings – Again

The Permian water sector is entering another formative phase. Infrastructure buildout, land positioning, long-haul transport corridors, and strategic permitting are once again central to competitive advantage. The difference is scale.

The Delaware Basin can no longer absorb its own water growth indefinitely. Pressure data and volume forecasts indicate that structural limits are forming. Companies that continue to evaluate disposal at the individual-well level risk missing the system-level shift underway.

Competitive advantage will accrue to those who understand pressure dynamics, anticipate regulatory inflection points, and design infrastructure across basin boundaries.